The 2014: Living in the Shadow of Regulation?

Whitepaper | Solutions

CONSEQUENCES AND CHALLENGES FOR BANKS

MINIMISING BUSINESS DISRUPTION

|

While there is a tremendous increase in regulatory activity, there is no specific framework for companies to follow in developing their regulatory response. Instead, companies should seek to create a new strategic framework of their own which would bring order and structure to the process

There are multiple global regulations seeking to achieve similar objectives but working on different timelines. Most organisations focus primarily on the differences across the regulatory landscape.

Identifying commonalities will prove helpful to banks first by identifying the regulatory elements common to various requirements across relevant geographies and addressing them through an integrated approach to avoid reworking, confusion and unnecessary costs.

Identifying commonalities will prove helpful to banks first by identifying the regulatory elements common to various requirements across relevant geographies and addressing them through an integrated approach to avoid reworking, confusion and unnecessary costs.

PRIORITISING INVESTMENT IN RESOURCE AND TRAININGMany banks will be putting large scale change programmes in place over the next two years to be compliant with and responsive to the regulations. However, as discussed in this paper, regulatory requirement will, by definition, make some parts of the business more costly and/or less profitable over time.

The cost of compliance is high and increasing rapidly, but those organisations that institute a centralised, strategic regulatory response programme will have more control over managing and optimising their investment in compliance.

IMPACT ON PROFITABILITY ON A RISK-ADJUSTED BASISThe introduction of so many new regulations means that banks will have to set priorities in order to be effective in terms of their responses. There are simply not enough resources, time, money or people to address every tactical aspect of every regulation.

For example, the Basel III/Capital Requirements Directive (CRD) IV provisions addressing capital requirements have a high potential impact on derivative transactions in particular, where higher levels of capital will need to be held to deal with the creditworthiness of the counter-parties also known as the CVA charge.

However, syndicated lending will experience relatively low impact since minimal funding is required, which can potentially be incorporated within the pricing.

understand this concept and make deliberate decisions about the trade-off between compliance costs and the costs of achieving an optimised state across the spectrum of required regulatory changes with the support of the business leads for priority strategic system and process enhancements. These choices will not be easy, but banks must establish priorities and determine what resources and funding will be needed to reach these objectives through the appropriate path.

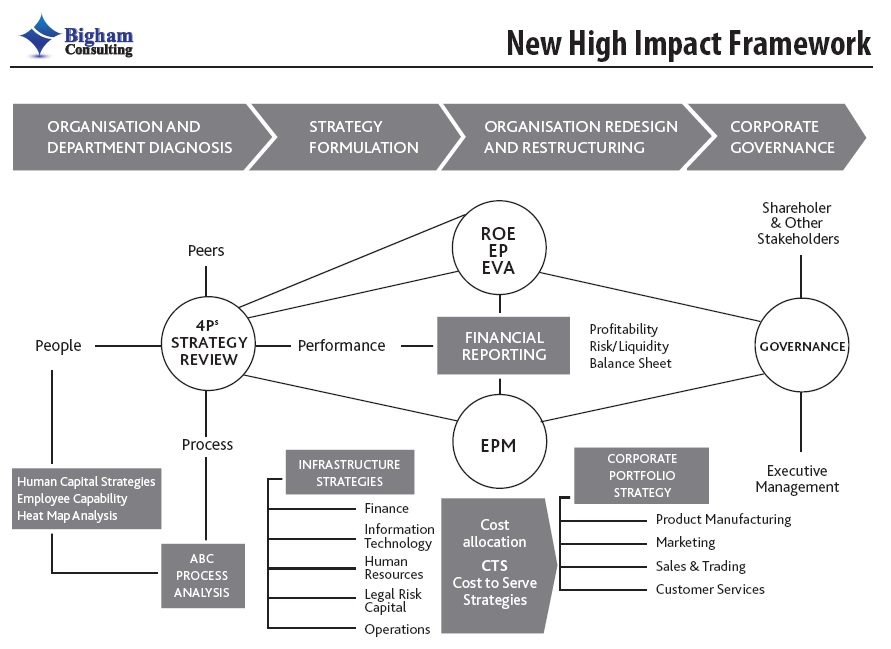

CREATE A FRAMEWORK TO TIE REGULATORY REFORM PROGRAMMES TO THE BANK’S OVERALL STRATEGYIdeally, the regulatory response becomes an integral component of the strategy, rather than a standalone initiative. One of the best approaches is likely to be organising complex regulatory demands into common themes for implementation.

Next week: Basic Approach

Here we conclude the over-regulation white paper in looking at a 4-stage strategy transformation approach that would help banks avoid running duplicating programmes and mitigate the cost of reform.

|